Don’t Budget, Spend Instead!

Executive Summary:

Common financial advice is for people to keep a budget of their spending. But budgets lead to people cutting back on their spending. Instead, spending should be encouraged. Spending money makes our lives enjoyable, both today and in the future. Spending intentionally on taxes, savings, and whatever else we need and want in life, leads to a more enjoyable life. Learn three spending strategies (values-based spending, needs before wants spending, and specific account spending) to turn monthly spending into intentional spending, so money goes where it brings the most joy and happiness.

Have trouble saving enough? Make a budget

Have too much credit card debt? Make a budget

Going on a trip soon? Make a budget

I prefer to avoid making budgets, and I think most people feel the same way. It feels like I am forcing myself to cut back on things. Why do I want to restrict my lifestyle with a spreadsheet I made?

Budgets force us to cut back on things. It is a lot like a diet. A diet reduces certain foods or cuts out what someone can eat. It is pretty common to see people starting on a diet and quickly struggling to maintain their progress. Budgets and diets both start the same way. With high motivation, but over time that motivation may decrease. Then we will be left with some rules we put on ourselves that we do not want to follow anymore. It is pretty easy from there to bend or break those rules.

Budgets work best for people who face large amounts of debt they cannot escape. Most people manage their finances well enough. Sure, people can spend less and save more, but is it sustainable to impose restrictions on how people want to live their life? I do not think so.

For most lawyers who want to make better financial decisions, I say, do not budget. Instead, spend!

Avoiding budgets seems counterintuitive to traditional financial advice, but it is not. Avoiding budgeting can be justified using two spending principles. First, we all have preferences. Some people prefer apples more than oranges, cars over trucks, and dogs more than cats. If you ask someone who does not like apples how much they would pay for an apple, they might say they would not pay anything. Likewise, if you ask someone who loves coffee how much they would pay for their favorite drink at their local coffee shop, they might even say a price higher than its current cost. We all have an internal set of values for everything in our lives, and these help us decide whether or not to buy something.

Second, it is much easier for someone to spend than to budget. Budgeting takes time to study past billing statements, categorize all of our spending, and then choose what to cut back on and how much to cut back. On the other hand, spending is easy. We spend money all the time. In my experience, it is tough to go a single day without spending money on something. So if we want to make better financial decisions, should we do something hard or something easy?

Life is hard enough. Make it easy and give yourself a chance to succeed.

How to Spend Intentionally?

Lawyers have a unique skill set that allows them to exchange their time for a significantly higher salary than the average American. Some lawyers may take a job in the public sector or work at a non-profit where they may make less than their private colleagues, but even these lawyers will make more than their non-legal coworkers. Lawyers with enough income to cover their bare minimum necessities then have options on spending their remaining money.

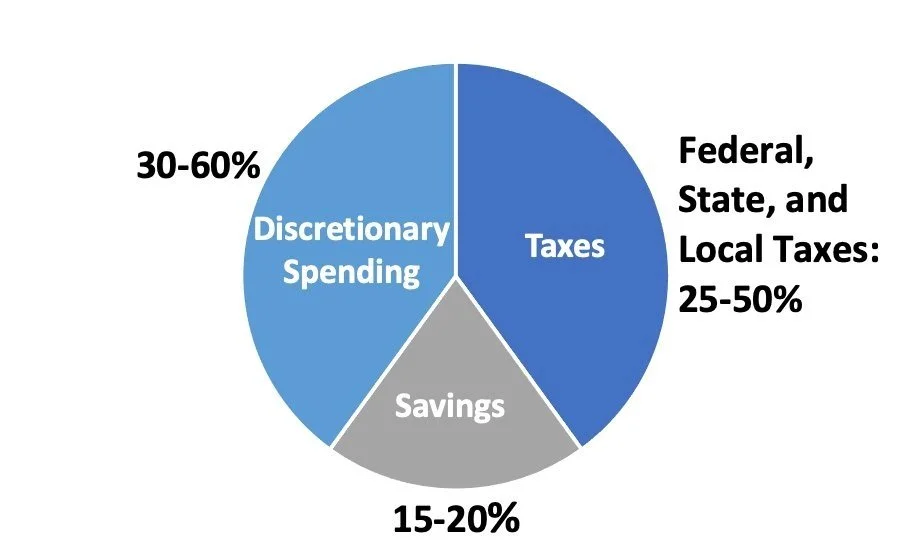

There are three major spending categories for lawyers:

Taxes (25-50% based on where a lawyer lives and their income)

Savings (15-20%)

Discretionary spending (Everything leftover)

Taxes

Each lawyer’s standard of living is different, but each requires some minimum level of spending to maintain. At a bare minimum, every lawyer will have one expense category they cannot ignore: taxes. Whether you are a lawyer living in a penthouse, a home in the suburbs, or with your family to save more money, everyone has to spend on taxes.

Taxes are the highest priority spending category because if you do not pay your taxes, you will be limited in what you can do in your daily life. It is safe to assume that Uncle Sam will always collect amounts owed to him. Taxes are also likely to be the largest single spending category in a budget. After accounting for federal, state, and local taxes, some lawyers will spend over 50% of their income on taxes alone.

Saving Before Spending

After taxes, saving money is the next most important part of any spending plan. In fact, for young lawyers, saving is a better way to build wealth than an optimal investing strategy. So how do we “spend” on savings?

The rule of thumb is that a lawyer should be saving 15-20% of their pre-tax income. A lawyer making $100,000/year should attempt to save $15,000-$20,000 per year.

When saving, people need to save for now and for later. Saving, for now, means establishing an emergency fund. Lawyers need to have a savings account worth 3-6 months of expenses. These savings should be in a savings account and not an investment account because you may need it for an unexpected expense or to pay the bills if you lost your job or could not work. When beginning to save, lawyers should put more savings towards their emergency fund than their investment accounts for the future. Protect your current self before helping your future self. A spending-related benefit of the emergency fund is that once fully funded, money that would have previously gone to the emergency fund can now all go towards saving for the future.

When saving for the future, lawyers have many different options:

Employer retirement plan like a 401(k)

Individual Retirement Account (IRA)

Traditional investment account (brokerage account)

The easiest way for a lawyer to save is through automatic paycheck contributions. Employer retirement plans like a 401(k) allow employees to assign a percentage of their income towards these accounts. Saving Hack: The 15-20% of savings include employer contributions. A lawyer with an employer match of 5% can achieve a 15% savings rate by contributing only 10% of their paycheck.

Lawyers just starting their career or those lawyers without an emergency fund would be better off if they contributed to their retirement accounts only up to the employer match percentage and the rest of the 15-20% towards the emergency fund. This strategy maximizes the employer match while allowing the most money to go towards the emergency fund.

Once the emergency fund is adequate, lawyers can increase their contribution percentage towards future savings to achieve the 15-20% savings rate. 401(k)s have an annual contribution limit (2022: $20,500). If a 15-20% contribution percentage exceeds that limit, lawyers can then contribute to their IRA until they reach that annual contribution limit (2022: $6,000). After these two tax-advantaged retirement accounts achieve their annual contribution limits, the rest of the 15-20% savings can go towards traditional investing accounts.

Discretionary Spending Strategies

As stated above, spending is easy to do. Budgeting is harder. These strategies will not involve calculating monthly grocery purchases to the cent. Instead, they focus on how we spend money and why we spend it. We all have a preference for different spending needs in our life. Once we figure out where the real value is in our lives, we can spend less on things that are not important and spend more on valuable items and experiences.

Values-Based Spending

We value different items and experiences differently. Maybe there are some expenses that you would love to spend on. Take a look back on where you spent your money last year. Where did you feel like you spent your money the best? Was it on experiences, gifts, products, or services? Then also look at where you spent money last year where the money was not well spent.

Now ask yourself, would your life be more enjoyable if you spent less on the things that did not bring value to your life and increased your spending on the items and experiences where you best spent your money? Do you think your life would be more enjoyable? How would you spend extra money if it was directed towards something you highly valued?

Whether it is shopping, traveling, spending time with friends and family, or anything else, spending should go towards the things that bring our lives the most enjoyment. So spend more on those things.

I like to travel and cook. For me, it is easy to spend $30 extra a week on organic groceries or uncommon ingredients I typically would not buy. It is the same for travel. I do not mind spending more on an Airbnb or dining and entertainment when I travel. I know I will look back on these experiences and be glad that I spent that extra money on something I enjoy.

Needs before Wants Spending

Have you ever been so thirsty you would pay five times more than a water bottle typically costs to quench your thirst? In that situation, the water bottle is not a want. It is a need! When you need that water, the other things you want in life do not disappear. Instead, the need for water becomes much greater than the desire for something you want.

By prioritizing spending from the highest priority needs to the lowest priority wants, lawyers will spend in a way that achieves the financial life that brings the most value.

Spending really can be as simple as spending on needs and using remaining income to spend on wants. Some needs that people commonly pay for are:

Food

Housing

Utilities

Transportation

Insurance

Debt payments

Wants are numerous and can even be a want to upgrade a need. Think about wanting to move to a house from an apartment or wanting to buy a new car. Some examples of wants are:

Entertainment

Dining out

Travel

Charitable Giving

Health and Fitness

Shopping

These wants can also be needs. For a lawyer who loves to exercise, maybe they need at least to pay for their monthly gym membership. But if they want to start paying for workout classes or a personal trainer, lump the gym membership in the needs spending and the workout classes or personal training in the wants spending.

Specific Account Spending

For lawyers who like to be more organized with their spending, try out the specific account strategy. The first step in implementing this strategy is to open bank accounts for different spending categories. The next step is to set up automatic transfers that send specific amounts to each bank account. Then a lawyer can spend the money in each account on whatever its spending category is. Once that bank account is at $0, the lawyer will have to wait until the next paycheck to spend any more on that category.

The number of accounts varies by person, and it can be as simple as a savings account, an investment account, a needs account, and a wants account. It can also be more complex. Some lawyers may prefer opening multiple accounts for different goals. Goals may include a down payment account, a new car, dining out, or shopping.

Example: A lawyer loves to eat out with friends. The lawyer decides they want to spend $400 each paycheck on eating out. As each paycheck arrives in their checking account, $400 automatically transfers to the dining out account. The lawyer can now go out to breakfast, lunch, and dinner with friends if they want. They can spend all of the $400 they want without feeling guilty or worried that they are spending too much. If the lawyer has $100 remaining in the dining out account when the next paycheck arrives, they now have $500 for dining out. Likewise, if the lawyer runs out of money in the dining out account before their next paycheck, they would not go out to eat until their next paycheck.

The separate account works well for lawyers who prefer an organized spending strategy. Setting up transfer amounts allows people to put a lot of spending towards the things they enjoy. If a lawyer does not enjoy traveling, they probably will not set up a traveling account. Lawyers who want to maximize their credit card rewards can also tie different spending accounts to credit cards that offer more points or cashback for that specific spending category (groceries, travel, dining out, etc.).

Tips and Tricks to Spend Better

The strategies above can help lawyers who want to spend their money better. Budgets can be restrictive. They have their place in financial planning, but I think more often than not that it is better to encourage intentional spending rather than restrictive budgeting. Here are a few tips and tricks to help lawyers spend better:

Save before spending

Reflect on what you like to spend on and ask yourself what life would be like if you spent even more on it. Then do it!

Not all needs are wants, and that is okay. No one likes paying for insurance or debt payments, but they are a critical part of any reasonable spending plan.

Break down spending into short periods like a monthly timeframe.

Automate transfers and auto-pay bills but check your statements regularly to ensure you are not paying for things you do not want or need.

Do not be ashamed of your spending. Spending is supposed to make your life better. If you intentionally spend on things that make your life more enjoyable, consider it money well-spent.

Try different spending strategies until you find one that works best for you.

The Developing Financial Process focuses on spending intentionally rather than budgeting restrictively. The spending plan is tailored to spend more on things that bring each of us joy. If you love to shop then let’s put more spending towards shopping. If eating at fantastic restaurants with fantastic friends and family adds tremendous value to your life, let’s spend more on dining out. Lawyers work so hard to earn their income so let’s use that money to make life as great as it can be. If you would like to see how spending more intentionally can lead to a better financial life, schedule a Meet & Confer and let’s see how the Developing Financial Process can benefit you. You do not have to spend anything for this Meet & Confer because the first two meetings are always free.

Disclaimer: Nothing in this blog should be considered financial advice or recommendations. Your questions are unique to you and your own personal financial circumstances. You should consult with a financial professional before making a financial decision. See full blog disclaimer.